Section 1: Introduction

Analysis of liability numbers is as important as keeping provisions for them. A company is advised to keep provisioning for long-term benefits payable to its employees using actuarial techniques so that it neither ends up with under-provisioning nor over-provisioning

liabilities. Actuarial methods to value the Present Benefit of Obligation (Hereinafter referred to as “PBO”) takes into consideration various inputs:-

• Employee data with their DOJ, DOB, leave balance, and current salary.

• Assumptions including salary escalation rate, attrition rate, discount rate, retirement age, mortality rates, and ceiling(if any).

Section 2: How to Analyse Liability Numbers?

The following are the key factors:

1. Comparison with Accrued values:

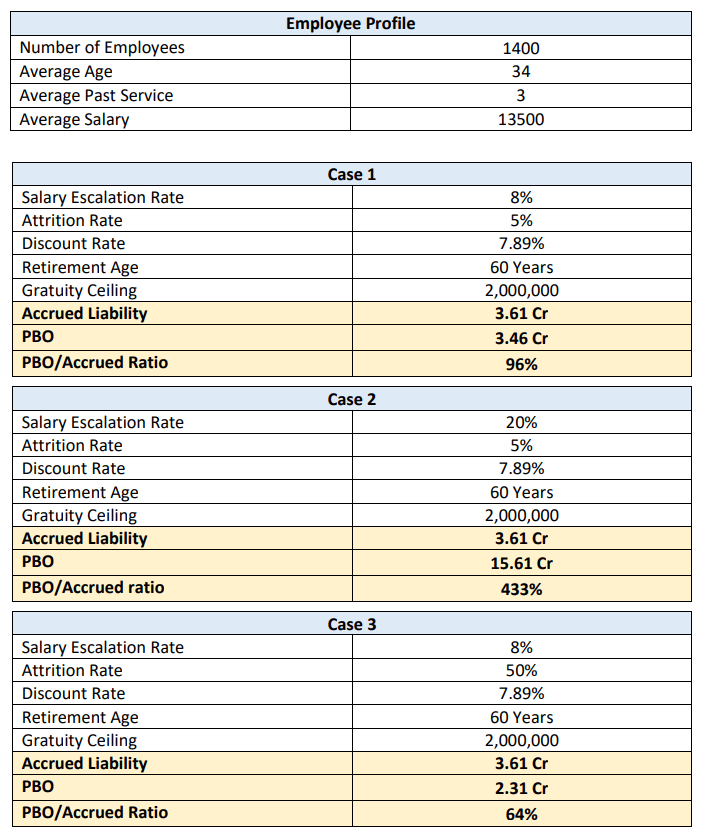

The first and most easy step in the liability numbers is to compare the estimated number with an accrued number. If the assumptions are in line with the industry, say (6-9)% salary escalation rate and (5-8)% attrition rate the PBO will come close to accrued in the majority of cases and the difference will be justifiable. However, if the assumption is an outlier, say (20-25)% salary escalation or/and (40-50)% attrition rate, the numbers will differ from accruing.

For example,

• Consider, company XYZ LTD for which we have to calculate gratuity liability. The benefit formula to calculate gratuity is 15/26 * Basic Monthly Salary * Completed years of service. The data for the company as of the valuation date:

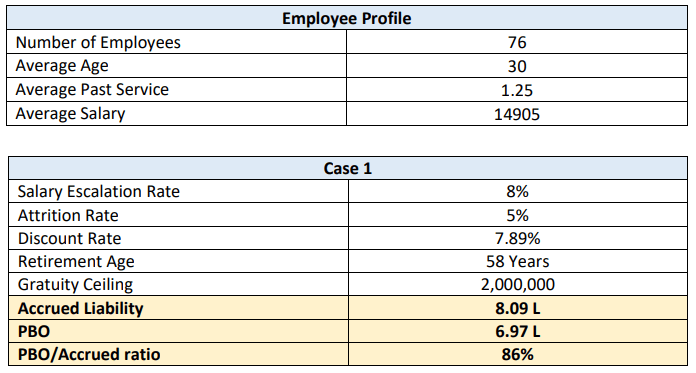

• Consider, A company ABC LTD for which we have to calculate gratuity liability. The benefit formula to calculate gratuity is 15/26 * basic monthly salary * completed years of service. The data for the company as of valuation date:

Here, accrued is more than PBO because the average past service is 1.25 and all the employees are under vesting period. Though Accrued numbers are good to start with due to variations in assumptions across companies, we need to consider many factors too.

2. Comparison with the Previous year’s PBO:

PBO values across two years should be consistent. The movement in the PBO over the year should be justified. The movement in PBO for two consecutive years is due to the following factors: –

Interest Cost:- Since we discount back our liabilities to the valuation date, we must carry forward the previous year’s liability by one year using the discount rate of the previous year’s valuation.

Current service cost:- Current service cost is the one-year cost to the organization, resulting from employee service in the current period. This value should be consistent with the previous year’s numbers if there isn’t any major change in assumptions or liability numbers in the employee profile of the company.

Past Service Cost:- Past Service Cost is the change in the PBO for employee service in prior periods, resulting in the current period due to any unanticipated change in the Act or laws. For example: recently the gratuity ceiling has increased from 10 lakhs to 20 lakhs due to which there is a major change in the liabilities of companies. Such change should go into past service costs. Actuarial Gain/Loss:- This is one of the most important components. Adding the above-mentioned components to the previous year’s PBO and deducting the benefit paid amount shall be equal to the current year’s PBO. If there is any change it will go into actuarial gain/loss. A surplus is a gain and a deficit is a loss. There are two components of actuarial gain/loss:

1. First, is due to changes in assumptions provided by the company. If the company has changed its assumption then there would be actuarial gain/loss depending upon the change. For example, an increase in salary escalation rate will increase the PBO and vice versa because employee benefit is payable using the salary in the last month of decrement(withdrawal, resignation, or death/disability) which has increased as compared to the previous year.

2. Second, is due to experience adjustments. A change in the actual experience as compared to the assumption made might result in actuarial gain/loss. Say, a company has expected to increase salaries by 7% but due to the good business it made in the year, salaries increased by 20%. This will result in actuarial loss due to experience adjustments. Take another example, where a company had 100 employees the previous year but due to a bad business in the year, it decided to fire 50 employees. The employees had not completed the vesting and hence no benefit was made to them however liability was kept in books a previous year and hence it will result in actuarial gain due to experience adjustments.

Section 3: Importance of Analysis of Liability Numbers

For an Actuary, numbers speak louder than words.

Numbers tell a lot about the accuracy of the valuation, assumptions, and data provided. If incorrect liability numbers are provided to the organization, it might result in under-provisioning/overprovisioning of liabilities and may be a risk to the organization.

For example, under-provisioning means that a company might not be able to pay off the liabilities as and when they arise. Similarly, over-provisioning will have an impact on the company’s profits.

If the PBO number shows a huge movement over a year, we should analyze it in the following steps:

1. First we should compare the data of the two years, the DOJ, and DOB should be the same as last year. In the case of leave valuation number of leaves should be consistent with past year leaves taking into consideration yearly accrual leaves and maximum accumulation. Also, the salary increase should be consistent with our assumption as well as last year’s salaries. If any major deviation is there it should be reported to the client and the reason should be asked for the change.

2. Second step should be to see a change in assumptions and analyze its impact. The new assumptions must be realistic as compared to the experience history of the company, if

available.

3. The third step should be to see if there is any other change that is affecting liability like a change in act, acquisition in/out in the case, or merger/demerger. If there is such a change it should be disclosed in the report.

4. PBO of last year of employees left during the year and benefits paid to them should be compared and any major difference should be justified.

5. Employee-wise liability of two years should be analyzed.

6. Liabilities of KMPs (Key Management Personnel) usually contribute a major share in the overall liability of the company. Any major change in their details may have a significant impact on the movement of liability. For example, a 40% salary increase for the director of a company will

increase PBO significantly.

By now we would have got enough reasons that justify the liability numbers and variation from the previous year and accrued values.

Disclaimer: This above note has been furnished solely for information and must not be reproduced or redistributed. This material is for the information of the recipient and we are not soliciting any action based upon it. Neither Mithras Consultants nor any person connected with it accepts any liability numbers arising from the use of this document. The above note is not providing any recommendations. The information

should not be relied upon as advice on your specific circumstances.

Call Us

Call Us

Whatsapp Us

Whatsapp Us